Mat Credit Entitlement Accounting

Significant Accounting Policies Mindtree

Significant Accounting Policies And Notes To The Accounts For The Year Ended March 31 2013 Mindtree

Standalone Financial Statements Mindtree

Consolidated Financial Statements Mindtree

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Consolidated Financial Statements Mindtree

A in the year of creation.

Mat credit entitlement accounting.

Minimum Alternate Tax

Http S2 Q4cdn Com 482484005 Files Doc Financials Quarterly 2019 Q1 Combined Financials Fy19 Pdf

India Glycols Ltd Fundamental Analysis Dr Vijay Malik

Https Www Dishmangroup Com Files Dishmangroup Investor Relations Carbogen 20amcis 20 India 20ltd Pdf

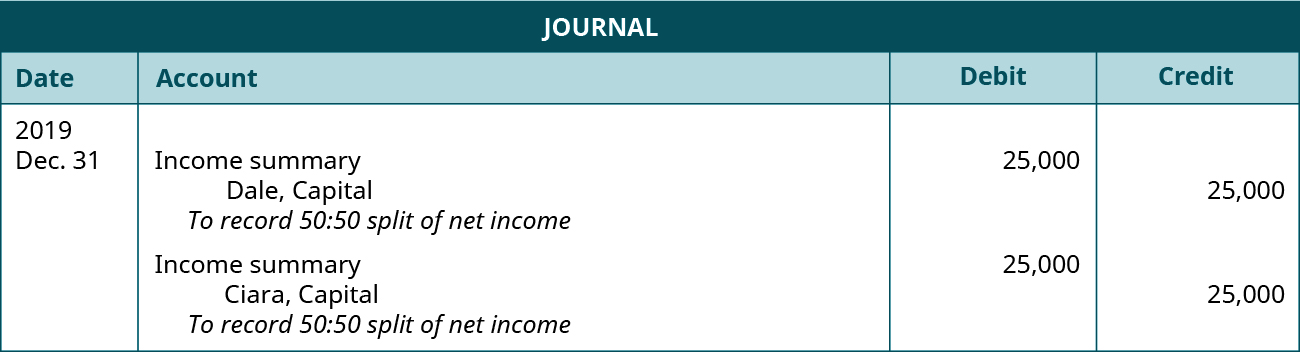

Compute And Allocate Partners Share Of Income And Loss Principles Of Accounting Volume 1 Financial Accounting

Https Cdn2 Hubspot Net Hubfs 5724847 Fy 19 Revamp Assets Website Investors 20 Investor 20financial 20information 20 20resource 20center Statutory 20information Singapore 20sub Mar19 20ind 20as Pdf

Http Www Bancoindia Com Wp Content Uploads 2018 05 Afrbpil2018 Pdf

Http Www Oracle Com Us Industries Financial Services Mantas India Private Ltd 2016 3179111 Pdf

Entries Archive Strategic Finance

Https Biocon Com Docs Biocon 20research 20limited 2019 Pdf

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

As 22 What Is Mat Credit Youtube

Scary Accounting Accountant Halloween Funny Mouse Pad Zazzle Com In 2020 Accounting Jokes Accounting Humor Accounting

Pdf The Pedigree Of Accounting In Kiribati And Its Consequent Prospects In The Transparency And Accountability Stakes Sponsored By The International Financial Institutions

Practitioner S Guide To Audit Of Small Entities Caalley Com

Http Www Aera Gov In Aera Upload Pb Ficci Pn 4 16 17 Pdf

Https Assets Kpmg Content Dam Kpmg In Pdf 2020 01 Chapter 1 Aau Tax Ordinance Pdf

Master Of Accountancy In Taxation Mat University Of Dhaka Marketing Jobs Independent Writing Business Studies

Https Shipindia Com Upload Financialresult Results Q1 19 201 Pdf

Https Egrove Olemiss Edu Cgi Viewcontent Cgi Article 1878 Context Aah Journal

Vedanta Ltd 2016 Foreign Issuer Report 6 K

Minimum Alternate Tax Mat Section 115jb

Https Sfmagazine Com Wp Content Uploads Historic 1980 1989 1989 11 Management Accounting V71 N5 Pdf

Pdf The Effect Of Creative Accounting On Audit Failure The Case Of Manufacturing Companies Quoted On The Nigerian Stock Exchange

Source : pinterest.com